How 50 insurance leaders uncovered 21 strategic blind spots — and what comes next

In an age of accelerating complexity, insurers face challenges unlike any before: a shifting climate, geopolitical uncertainty, exponential technologies, and evolving societal expectations. Strategic foresight is no longer a luxury—it is a necessity.

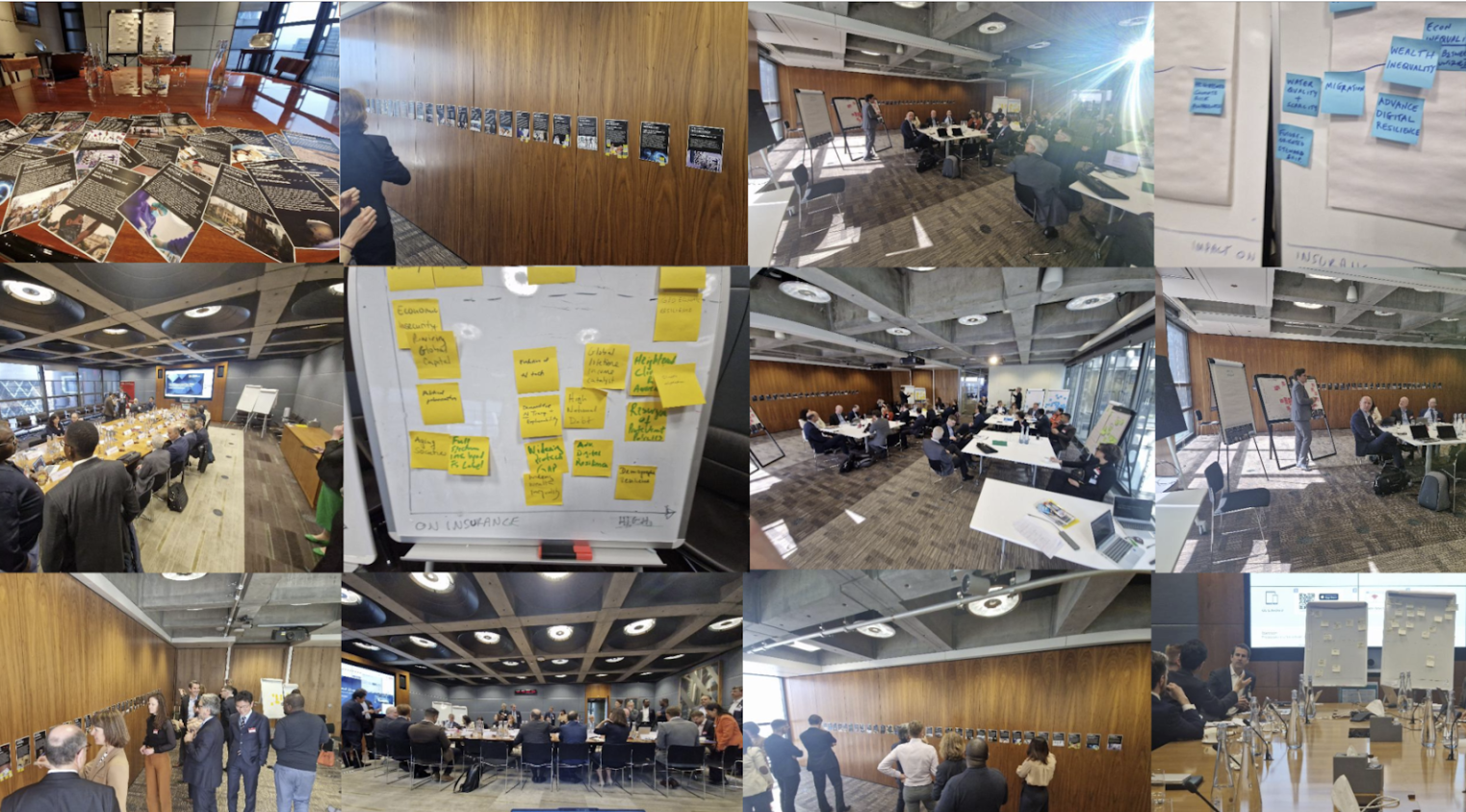

In April 2025, The Geneva Association convened a high-level foresight workshop in London, facilitated by Vincent Defour, CEO of Trendtracker, with the participation of its Research Associates and Key Correspondents.

In the past Trendtracker has supported The Geneva Association with internal and external workshops to facilitate similar foresight expert workshops

"It was extremely insightful to identify blind spots, supported by AI, discussing in peer groups with diverse backgrounds." - Lukas Ziewer, Group Chief Risk Officer at Athora.

This longread captures the insights, blind spots, and strategic priorities identified during two days of collaborative exploration.

Trendtracker: an AI-powered foresight platform built for strategic decision-making

Trendtracker is a fully AI-powered foresight and strategic intelligence platform. Unlike traditional methods that rely on manual expert opinion, Trendtracker leverages proprietary AI, deep analysis, real-time data analytics and automated scoring to identify disruptions before they go mainstream.

Our platform acts as an always-on radar—helping decision-makers:

- Anticipate threats and opportunities.

- Avoid strategic blind spots.

- Act with confidence and clarity.

We work with Fortune 500 companies, financial institutions, and consultants globally to strengthen their futures through rigorous, data-driven foresight.

“Trendtracker serves as a good guide to help us steer through an ever-growing maze of options and complexity in a fast-changing world.”

— Hans De Cuyper, CEO Ageas

The ways the Geneva Association is reshaping insurance research through foresight

The Geneva Association, founded in 1973, is an international association of insurance company leaders, which includes CEOs of both insurance and reinsurance firms. It is known as the insurance sector's think tank, and it is dedicated to conducting comprehensive research in collaboration with its member companies, academic entities, and various global organizations.

The Geneva Association is currently resetting its research architecture for 2026–2027. In this cycle, it seeks to:

- Encourage cross-silo thinking beyond individual workstreams.

- Co-create topics with GA Associates and Key Correspondents.

- Use foresight methodologies to guide its research roadmap.

To support this evolution, Trendtracker facilitated a structured two-day workshop, using tools like Uncertainty Mapping, and Blind Spot Analysis to align and prioritize the next wave of strategic topics.

How blind spot mapping helps insurance leaders spot what others miss

A Blind Spot Mapping exercise helps organizations uncover strategic areas they may be ignoring, underestimating, or misjudging—typically due to bias, outdated assumptions, or internal silos.

The concept of blind spot mapping has its roots in cognitive psychology and behavioral economics, where researchers identified how human decision-makers tend to overlook disruptive signals due to confirmation bias, groupthink, and escalating commitment. These blind spots—areas we don’t see or choose to ignore—can lead organizations to persist with outdated strategies even in the face of profound external change.

The technique was later adopted into strategic foresight and systems thinking as a method to visually contrast internal assumptions with external realities. Over time, it has evolved into a powerful diagnostic and planning tool, particularly for industries like insurance that operate in highly uncertain, complex environments. By surfacing these hidden gaps, blind spot mapping enables leaders to confront uncomfortable truths—and design strategies that are more adaptive, resilient, and future-ready.

Inside the blind spot mapping process

- Internal view: Evaluate current strategy and dominant beliefs.

- External view: Assess disruptive macro forces.

- Compare results: Identify contradictions.

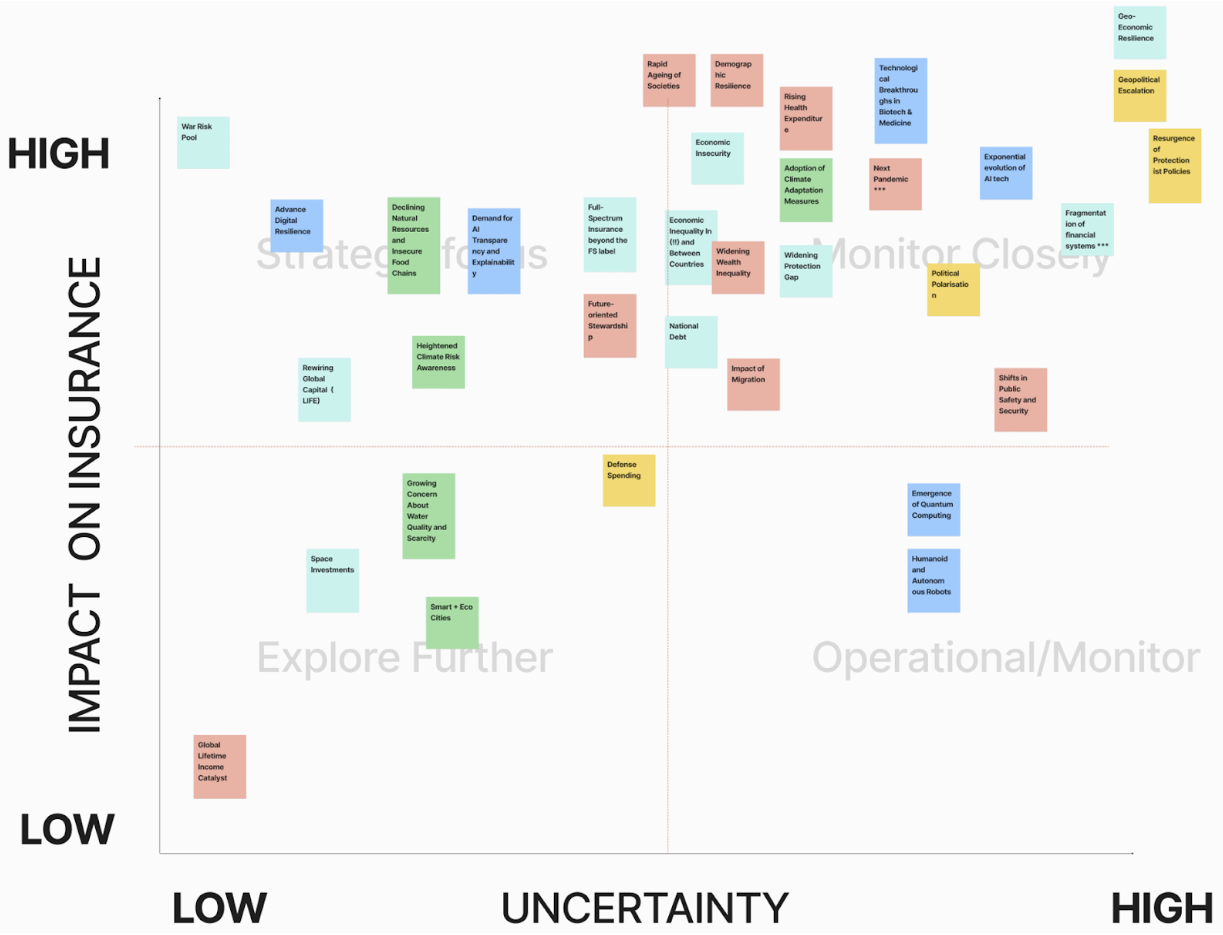

- Visual mapping: Place insights on a 2x2 grid (Impact vs. Scope).

The strategic value of spotting what others miss

- Reveals unseen vulnerabilities.

- Highlights innovation opportunities.

- Sharpens executive focus on long-term uncertainty.

- Reduces overconfidence in flawed assumptions.

This methodology helps leaders make more resilient, future-aligned decisions.

From 300 global risks to 21 blind spots: how AI foresight shaped the workshop

Before the in-person workshop, Trendtracker deployed its AI foresight engine to scan, score, and prioritize over 300 potential blind spots across global macro forces—spanning the PESTEL dimensions: Political, Economic, Social, Technological, Environmental, and Legal.

These macro-level risks were mapped across three core insurance lines: Life, P&C, and Health, and linked to key segments of the insurance value chain—from underwriting and pricing to claims and investment management.

Each risk was scored based on quantified impact, uncertainty, and speed of emergence, then aligned with major shifts seen across the portfolios and operating models of global insurers. This produced a pre-filtered selection of high-signal risks, which served as the foundation for the human-machine foresight process used during the workshop. Out of the 300 analyzed risks, Trendtracker generated a shortlist of the most strategically relevant candidates, from which 21 final blind spots were selected in co-creation with Geneva Association members.

For example, "Underfunded Pension Systems" was flagged as a critical blind spot for Life insurers. While often treated as a known issue, Trendtracker's models showed its compounding interaction with demographic decline, inflation, and social trust erosion—making it a systemic vulnerability rather than a background trend. It not only affects annuity markets but also calls into question insurers' roles as societal safety nets.

Another example, "Digital Divide in Financial Access", emerged as a blind spot for Health and P&C insurers seeking to expand inclusion. As insurers embrace digital-first distribution, underserved populations risk being excluded due to lack of infrastructure, digital literacy, or affordability. This digital access asymmetry could create significant inequality in coverage, which both regulators and social movements are increasingly scrutinizing.

In the P&C space, "Climate Policy Divergence"—where countries adopt vastly different regulatory approaches to decarbonization—was scored as a blind spot with cascading effects. It affects risk modeling, cross-border investment decisions, and the competitiveness of multinational insurance products. Trendtracker linked this blind spot to underwriting inconsistencies and reputational risk for global insurers navigating climate-conscious markets.

Lastly, "Trade Wars & Economic Sanctions" was identified as a critical blind spot with potential to undermine global capital flows, reinsurance structures, and supply chain stability. These disruptions could fragment risk pools, destabilize premium flows, and elevate counterparty risk in cross-border deals. For insurers operating internationally, it challenges the very foundations of portfolio diversification and financial resilience.

By automating the early detection and scoring of these threats, Trendtracker reduced cognitive bias, improved strategic alignment, and enabled The Geneva Association and its members to concentrate their efforts on the most actionable foresight priorities.

Together with the research team of the Geneva Association 21 Blind Spot were withheld to be used in the workshop.

Inside the Geneva Association’s foresight workshop in London

Held in April 2025, the workshop at the Lloyds Building in the financial centre of London, brought together Geneva Association Associates and Key Correspondents for a deep, participatory foresight experience. In total 50+ participants from different global insurance industry leaders joined the different workshops.

The Geneva Association's membership consists of Chief Executive Officers (CEOs) from the world's leading insurance and reinsurance companies. Currently, there is a statutory maximum of 90 members, all of whom are CEOs of major international insurance and reinsurance firms. The association serves as a think tank, conducting research and facilitating discussions on key issues facing the insurance industry.

Some Members are Achmea, Aegon, Ageas, Allianz, Aviva, AXA, Generali, Groupama, Hannover Re, NN Group, Munich Re, Prudential (UK), Swiss Re, Unipol, Zurich, Converium, Fortis, ING, Prudential, Winterthur, …

Foresight workshop overview

Day 1: mapping uncertainty to prioritize high-impact risks

- Plotted Blind spots by Impact and Uncertainty.

- Used to identify blind spots with disruptive potential and strategic priority.

Day 2: uncovering strategic blind spots through internal–external comparison

- Diagnosed where internal perspectives clash with external signals.

Mapped blind spots to identify impact and part of strategic plans of insurance companies to reveal hidden risks and overlooked innovation zones.

Key outcomes: a ranked blind spot map and research priorities for 2026–2027

- A ranked Blind Spot Map and consolidated conclusions cross

- 21 cross-group blind spots

- Shortlist of research themes with proposed questions

Example output:

The most disruptive blind spots insurance leaders identified in the workshop

High-Impact Blind Spots

During the foresight sessions, participants surfaced a core set of high-impact blind spots—critical areas of disruption that demand strategic attention from insurers. These risks, spanning from technology to geopolitics, were selected due to their potential to reshape risk landscapes, product portfolios, and societal expectations.

- Demand for AI Transparency and Explainability

Description: Stakeholders increasingly require clear, interpretable decision-making from AI systems.

Why it matters: Insurers using opaque models face regulatory risk and potential erosion of trust. - Exponential Evolution of AI Tech

Description: AI capabilities are advancing toward autonomy and deep integration into business systems.

Why it matters: Legacy risk models may become obsolete, while AI-driven tools could introduce new liabilities. - Smart + Eco Cities

Description: Urban centers are evolving into data-rich, sustainable, and sensor-dependent ecosystems.

Why it matters: Insurers must reimagine products and services to cover new infrastructure and lifestyles. - Widening Protection Gap

Description: Vulnerable populations continue to lack access to basic financial and risk coverage.

Why it matters: This threatens the social role of insurance and exposes gaps in business models. - Advanced Digital Resilience

Description: Systemic digital risks—from cyberattacks to infrastructure failure—are increasing.

Why it matters: Insurers must not only offer cyber coverage but protect their own digital core. - Heightened Climate Risk Awareness

Description: Stakeholders now expect action—not just recognition—on climate adaptation and mitigation.

Why it matters: Insurers face growing pressure to underwrite responsibly and support resilience efforts. - Geo-Economic Resilience

Description: Strategic competition is reshaping globalization, with a focus on economic sovereignty.

Why it matters: Fragmented trade and finance systems challenge cross-border risk pooling and capital flows. - Economic Inequality (in/between countries)

Description: Wealth disparities are deepening across and within nations.

Why it matters: Social instability, lower insurance penetration, and rising claims burdens could follow. - Technological Breakthroughs in Biotech/Medicine

Description: Innovations are transforming longevity, disease management, and diagnostics.

Why it matters: New risks and product opportunities emerge, especially in Life and Health insurance. - Geopolitical Escalation

Description: Global tensions and conflicts are intensifying, threatening multilateral cooperation.

Why it matters: Insurers face greater exposure to conflict-related claims and market volatility. - Fragmentation of Financial Systems (wild card)

Description: A collapse in global financial cohesion due to competing regulatory regimes or digital currencies.

Why it matters: Could destabilize capital access, reinsurance flows, and systemic risk frameworks. - Next Pandemic

Description: Future pandemics could emerge faster and with new social/economic dynamics.

Why it matters: Insurers must prepare for health, business interruption, and liability impacts beyond COVID-19. - Political Polarisation

Description: Increasing ideological divides are eroding institutional stability and policy coherence.

Why it matters: Weak governance environments complicate risk assessments and strategic planning. - Shifts in Public Safety and Security

Description: New threats—cybercrime, civil unrest, climate migration—are redefining societal safety.

Why it matters: Insurers must evolve coverage and claims frameworks to address emerging risk profiles.

Strategic research priorities for 2026–2027 shaped by the blind spot workshop

Based on group exercises and voting, the following key research areas were proposed:

⭐ Widening Protection Gap

Focus: Health, longevity, mortality, and income security

Strategic Relevance:

Despite global economic growth, millions remain uninsured or underinsured—particularly in health and life insurance. Aging populations, informal labor markets, and rising healthcare costs are widening the divide between those who can access risk protection and those left behind. This threatens the core purpose of insurance: enabling financial security and social resilience. As public systems strain, private insurers are expected to step in—but this requires new models for inclusive, affordable, and accessible coverage.

Key Questions:

- What are the underlying drivers of the protection gap across different demographics and geographies?

- Where can insurers apply innovative business models (e.g., microinsurance, embedded insurance) to expand access?

- What global partnerships or policy frameworks can support a shared approach to financial inclusion?

⭐ Exponential AI Evolution

Focus: Agentic AI, ethics, and risk modeling

Strategic Relevance:

AI is no longer just a back-office automation tool—it is evolving into a decision-maker. Agentic AI systems, capable of acting autonomously, raise profound questions around ethics, accountability, and risk. For insurers, this impacts everything from underwriting and pricing to claims automation and fraud detection. But with these advances come uncharted exposures and liability questions. The industry must prepare not only to use AI but to insure AI—while staying ahead of regulation and societal expectations for transparency and fairness.

Key Questions:

- How is AI transforming core insurance functions across the value chain?

- What governance and oversight structures are needed for AI-enabled operations?

- How can insurers model and underwrite emerging AI-driven risk classes?

⭐ Smart + Eco Cities

Focus: Urban risk transformation and ESG futures

Strategic Relevance:

Cities are becoming intelligent, interconnected ecosystems—with embedded sensors, renewable grids, autonomous mobility, and circular economies. These shifts bring immense opportunities but also systemic risks. Climate resilience, cybersecurity, energy dependencies, and social infrastructure all interact in complex ways. Insurers will need to develop tailored products and urban-level analytics to address a dramatically different landscape of physical, digital, and environmental risks.

Key Questions:

- What new insurance needs emerge in next-generation urban centers?

- How can insurers support sustainable infrastructure through innovative underwriting and pricing?

- What role can the industry play in incentivizing resilience in smart city design and governance?

⭐ Rewiring Global Capital

Focus: Capital with purpose, decarbonization, pensions

Strategic Relevance:

Insurance companies are among the largest institutional investors globally. As the financial system undergoes a profound shift toward decarbonization, equity, and long-term value creation, insurers must transition from passive capital allocators to active stewards of systemic resilience. This includes rethinking how portfolios are structured, where capital is deployed, and how impact is measured. The convergence of financial and social mandates requires insurers to lead—not follow—on the global capital transition.

Key Questions:

- How can insurers align investment strategies with long-term societal outcomes?

- What policy frameworks support “capital with purpose” without compromising fiduciary duty?

- How can insurers unlock capital to close pension gaps and finance the green transition?

⭐War Risk Pool

Focus: Conflict zones, public-private partnerships, systemic risk

Strategic Relevance:

Traditional insurance models typically exclude war, civil unrest, and geopolitical volatility. Yet, these risks are escalating and increasingly interconnected with cyber, infrastructure, and supply chain exposures. The emergence of hybrid threats and gray-zone conflicts exposes a protection vacuum. A multilateral war risk facility—co-developed by insurers, reinsurers, and governments—could help mitigate systemic disruption. Insurers must rethink their engagement with conflict-prone regions, both from a liability and resilience standpoint.

Key Questions:

- What innovative insurance mechanisms can absorb conflict-related risks?

- How can public-private partnerships be structured for high-severity, low-predictability threats?

- What governance models ensure fair burden-sharing and risk transfer?

⭐ Social Unrest

Focus: Societal fragility, inequality, systemic overlap

Strategic Relevance:

Inequality, distrust in institutions, and generational frustration are fuelling a surge in political unrest, protest movements, and civil disobedience. These social pressures often overlap with climate impacts, economic insecurity, and digital misinformation—creating compound crises. Insurers risk massive exposure in the form of property damage, business interruption, and reputational loss if social volatility is not factored into future strategies.

Key Questions:

- How can insurers model, price, and hedge against social instability?

- What role can inclusive insurance models play in reducing systemic fragility?

- How might insurers support communities in post-unrest recovery and resilience building?

⭐ AI-Cyber Convergence

Focus: Complex liability, emergent exposure

Strategic Relevance:

As AI systems integrate into critical infrastructure, they also become targets—and agents—of cyber risk. From autonomous vehicles to AI-managed utilities, any disruption could have cascading effects. Yet, liability remains murky. Who is responsible when an AI fails due to a cyber breach? Current coverage models are not equipped for these intersections. Insurers need to define new risk categories, standards of care, and policies that cover AI failures, cyber sabotage, and downstream losses.

Key Questions:

- Where do AI and cyber risks intersect, amplify, or create new liabilities?

- How should insurers underwrite and price policies for AI-enabled systems?

- What regulatory changes are needed to clarify legal responsibilities and insurability?

What comes next: strategic research themes for 2026 and beyond

The Geneva Association’s London foresight workshop demonstrates the power of collaborative intelligence. By integrating AI-powered tools with strategic insight from industry leaders, it is possible to:

- Align on emerging macro forces

- Identify and mitigate critical blind spots

- Shape an evidence-based, future-ready research agenda

As insurance enters a decade of disruption, those who embrace foresight will be better positioned to protect people, assets, and society in bold and transformative ways.

Ready to map your own blind spots? Our strategy experts are ready to support you and walk you through Trendtracker.